22nd March 2019

Outside Fortress Europe Excerpts

This Global Business Strategy Blog post is based upon unabridged excerpts from Chapter Five, Analysing Global Markets and the Intelligent Company, in Outside Fortress Europe: Strategies for the Global Market.

Context References

Beioley, K. (2019, February 8). Woodford named in list of poor performing ‘dog funds’. ft.com.

Murphy, H., & Spero, J. (2018, June 22). Neil Woodford fires back over Stobart-Flybe ‘deal’ claims. ft.com. Smith, P., & Beioley, K. (2019, March 15). Woodford accuses investors who quit his funds of ‘appallingly bad decisions’. Financial Times, p. 1.

Smith, P., & Beioley, K. (2019, March 15). Knives are out for fund manager Woodford: Investors angry, short-sellers on the alert and rivals enjoying the show – but the UK stock picker is fighting back hard. Financial Times, p. 15.

Outside Fortress Europe Excerpt

Introduction

Traditional financial economics argues that it is impossible for investors to ‘outperform’ asset markets, a theorem known as the Efficient Market Hypothesis (EMH). In this section we will demonstrate that, while this may or not be the case for individual investors or fund managers, deep market analysis, insightful information processing, astute knowledge management, a sharp customer focus and penetrative differential advantages enable intelligent companies to break this fundamental economic rule.

Market knowledge and the strategy payoff: the intelligent company

I can calculate the motions of heavenly bodies but not the madness of money.

Sir Isaac Newton (1643-1727).

Mathematician, physicist, astronomer, theologian etc.

Numerous scholarly research projects (and some frankly frivolous but fun experiments involving Florida ‘seniors’ and, separately, monkeys) have demonstrated that highly-paid Wall Street and City of London fund managers are not worthy of the generous remuneration packages they receive. In both finance and economics, behavioural sciences are in the ascendency, challenging fundamental theorems associated with the EMH (see Malkiel, 2016, for an update on his original ‘Random Walk’ thesis) and other aspects of behavioural economic life, perspectives ranging from Nobel-laureate-academic (Thaler, 2016) to lightweight-facetious (e.g. Levitt and Dubner, 2007). Also, please take note of John Maynard Keynes’s oft-cited comment that “the market can stay irrational far longer than you or I can remain solvent”.

(Monkeys are frequently used in experiments relating to ‘stock-picking’ to challenge the idea that any individual investor – or highly-paid fund manager – can outperform the stock market by being smarter than the animal; time-after-time, the monkey wins. Applying this concept to Donald Trump’s hotel, casino and resorts business for the decade following 1995, Warren Buffet observed: “If a monkey had thrown a dart at the stock page, the monkey, on average, would have made 150%”. Investors in Trump’s business, he noted, lost 90 cents on every dollar during the same period).

In the real world, and as was discussed earlier, two Nobel prize-winning economists, Robert Merton and Myron Scholes, brought the global financial system to the brink of meltdown during their Wall Street adventure with Long Term Capital Management (LTCM) in 1998. The following quote from one of the professors, Myron Scholes (cited in Lowenstein, 2001), demonstrates the extraordinary self-belief of the ‘quants’, as they are affectionately known in the business:

What we do is look around the world for investments that we think are, because of our models, undervalued or overvalued. And then we hedge out the risk of something we don’t know, like a market factor.

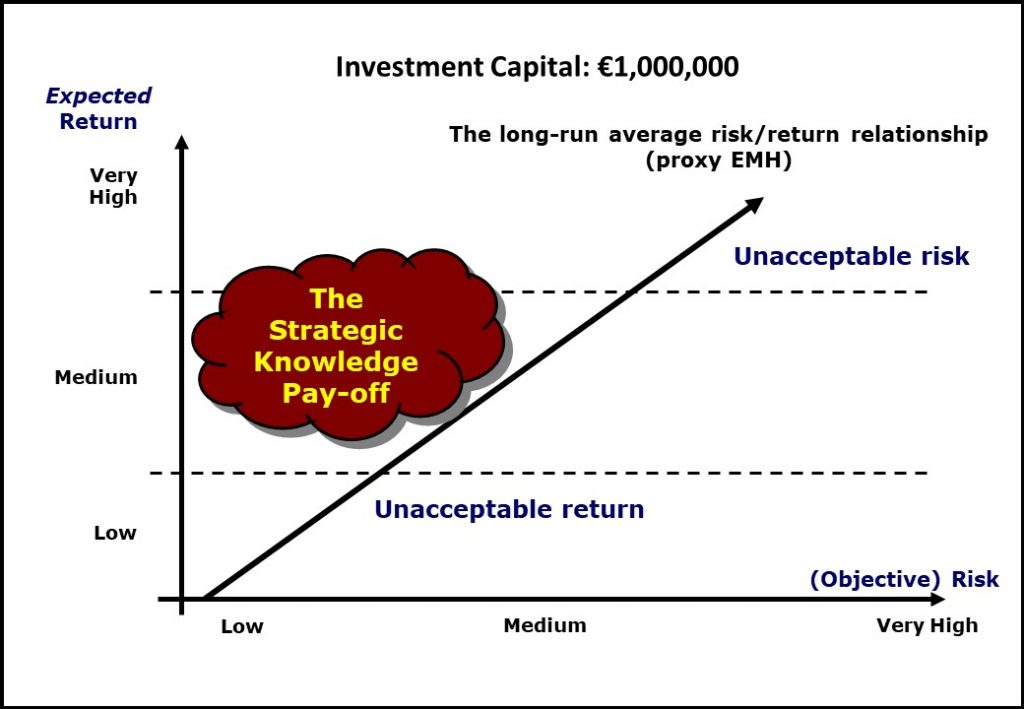

Figure 1 below presents a proxy for EMH, graphically demonstrating the three interacting elements of finance and investment theory: (i) Investment; (ii) Risk; (iii) Expected Return.

Let’s assume that investment capital is a fixed amount, say, €1m. Risk is presented here on the horizontal axis as an objective factor, a proxy for broader market acceptance of the risk associated with any asset class or asset portfolio. The reason for the emphasis on expected return as depicted on the vertical axis of Figure 1 relates to the behavioural dimension of investment theory, i.e. it describes the motivation underpinning the investment decision made by an individual or group of like-minded investors. So, for example, why would someone invest in a very high-risk project?

-

-

- Cynically stated, because they’re greedy, like fictional character Gordon Gekko (“greed is good”) or the very real Jordan Belfort, the Wolf of Wall Street (Belfort, 2007; and movie with the same title, 2013).

- Or they have animal spirits, “a spontaneous urge to action” (attrib. John Maynard Keynes).

- Or they think they’re smarter than the market (e.g. Profs. Merton and Scholes of LTCM).

- Or they’re deluded.

- Or, less critically, because they know what they’re doing, can afford to play the game and are prepared to lose their money (e.g. Wayne Rooney).

-

Such motivations and variations upon them have been the defining characteristics of every boom-and-bust bubble in economic history, from 17th-century Dutch tulips (but see Goldgar, 2008, for a more balanced perspective than the typical hype associated with ‘tulip mania’) to 2018 cryptocurrencies such as bitcoin.

Reverting to Figure 1, we have refrained from naming specific asset classes here, but we can provide generalised examples along the horizontal (objective) risk axis, from lowest to highest:

Low: the lowest-risk asset class in this category is sovereign debt (bonds) issued by stable, advanced countries, e.g. US Treasuries, UK Gilts, German Bunds, French OATs etc. Cash-in-the-bank is the most common ‘mass-market’ example in this category, but it comes with a caveat: the principle of moral hazard applies and the notion that banks must be allowed to go bankrupt to constrain their lending behaviour is more likely since the 2008 financial crisis. Because of this, and to protect and placate their citizens, most advanced liberal democracies guarantee a ‘security blanket’ of a specified amount (e.g. £85,000 in the UK, €100,000 in the EU) and savers can (and should) spread bank bankruptcy risk across multiple independent qualifying institutions if they have available cash that exceeds these limits. ‘Blue-chip’ corporate bonds (debt) would also feature within this low-risk spectrum, towards its higher end.

Note that there are no zero-risk reference points in Figure 1. This is not a PowerPoint error: throughout Japan’s ‘lost decade’ during the 1990s, savers, in fear of deflation and/or bank failure, were putting their hard-earned ¥s under the mattress rather than depositing them in the bank. But even Japan has burglars; and very small dogs.

Medium: the typical profile here would be of a balanced, diversified portfolio of cash (for liquidity), bonds (for income) and equities (for liquidity, income and capital gain). The biggest risk investors take here is the potential loss of capital. A large majority of the general public will be invested in this risk category, primarily through their long-term savings for retirement and mostly through statutory pension funds. Most ‘active’ fund managers will earn their living from managing these investment portfolios and the most visible expression of them will be referenced to a stock-market index, e.g. FTSE 100/250, Dow Jones, S&P, CAC, DAX, Nikkei, Nasdaq etc. Taking the US as an example, blue-chip, dividend-paying, relatively safe (‘old economy’) companies are typically listed on the S&P 500, while the FAANGs (Facebook, Apple, Amazon, Netflix, Google – now Alphabet), represent riskier, higher growth-focused companies and are primarily listed on Nasdaq. Some commentators would put gold in this medium-risk category – it pays no income and its capital value can fall; however, it is the original hedge against inflation and the vagaries and volatilities associated with other asset classes and there are different means to access it, e.g. directly owning (and safely storing) ‘physical gold’ or owning shares (equities) of gold mining companies.

Very High: tulips from Amsterdam (Dash, 2010; and fictional movie, Tulip Fever, 2017); the millennium dot.com casino (Cassidy, 2002; Lowenstein, 2004); the sub-prime slice & dice (Lewis, 2010; and docudrama movie, The Big Short, 2015); the bitcoin bonanza; the unquoted biotech-equity stock-picker; etc.

Another way of presenting this spectrum of risk profiles is (low to high): savings – investment – speculation. But please note that the discussion thus far reflects the options available to an investor, whereas our focus in this book is on investment decisions made by executives on behalf of a typical company developing global business strategies. But these, in turn, rely upon and are constrained by investors and banks, so the principles remain the same.

The constraints on company capital investment decisions are reflected in Figure 1 by the dotted horizontal lines which represent the limits of corporate decision making: too low a promised return and the rational investor would deposit their capital in the bank; too high a perceived promised return and the typical investor would seek more mainstream investment opportunities.

Over and above these common-sense assumptions, most fund managers (and pension trustees) are prohibited either by law, prospectuses or ‘standing orders’ from making certain types of investment, for example, the percentage of an investment trust which can be allocated to riskier unquoted equities. We conclude this discussion of ‘the madness of money’ with another pithy observation from Warren Buffet: “I will tell you how to be rich. Close the doors. Be fearful when others are greedy. Be greedy when others are fearful”.

Returning to the theoretical world of financial economics, while we acknowledge both the principles of EMH (Malkiel, 2016) and the ‘irrational exuberance’ of markets identified by Nobel Laureate Robert Shiller (2016), we argue that, from a global strategic management perspective, it is indeed possible to outperform the market and ‘beat’ the long-run average return indicated in Figure 1. With this assertion, we pay tribute to no less an authority than Plato, who observed that “A good decision is based on knowledge, not numbers”.

This ancient observation, when considered in the contemporary context of ‘Big Data’, draws attention to another quote on the subject from esteemed (and honest) Nobel prize-winning economist, Professor Ronald Coase: “If you torture data enough, it will confess to anything”.

Keeping a keen eye on the prize depicted in Figure 1, The Strategic Knowledge Payoff, in the remaining sections of this chapter we explore multiple dimensions of effective information management, presenting numerous categories of information essential to compile for global business strategy success and for the intelligent company to outperform the market. The narrative will be minimal, but the logical flow of categories should be self-explanatory. Cross-references to other chapters and sections of the book are provided where appropriate.

Beyond data: big, small and nano-minutiae

Consider the following as a continuum:

-

-

- Business issue identification (opportunities, threats, key success factors).

-

-

-

- Data (processed).

-

-

-

- Information (compiled).

-

-

-

- Intelligence (analysed).

-

-

-

- Knowledge (interpreted).

-

-

-

- Global business strategy decisions (evidence-based).

-

-

-

- Performance (outcomes).

-

Successful mastery of these seven elements of market analysis gives the potential returns within the ‘The Strategic Knowledge Payoff Cloud’ illustrated in Figure 1. Technically, any investment/return to the left of the EMH proxy line in Figure 1 outperforms the market, but what we have demonstrated here is that the potential to achieve such a favourable outcome is confronted by the constraints imposed by financial markets and those investors who participate in them (see Kay, 2016, for an accessible and critical appraisal of financial markets and the financiers who work within them, primarily on behalf of others but always with a large dose of self-interest).

As a final observation relating to the central theme of this chapter section, there are two additional ways that an individual investor can outperform equity markets, each of which has a potential downside.

First, a company can legitimately offer its employees a discount on its shares as part of their remuneration which, by definition, will give them a market advantage in that particular company’s stock. The downside here arises if the equity is underperforming in its sector/stock market: the rational employee would demand the cash and invest in a different company, maybe a more successful competitor!

Second, the investor can trade on ‘inside information’, for example, their unique knowledge of an upcoming product launch or a potential project failure. And the downside?

Jailtime.

Recommended resources for further inquiry

For readers interested in exploring corporate finance and investment decision-making in more detail, the author’s recommended textbook, based upon the multiple criteria presented in the ‘Introduction to the Global Business Strategy Blog’ and extracted here is Pike et al. 2018, Corporate Finance and Investment: Decisions and Strategies.

The definitive book which aligns marketing strategy decisions with investment theories and shareholder value is Doyle, 2008, Value-based Marketing: Marketing Strategies for Corporate Growth and Shareholder Value.

Outside Fortress Europe Excerpt References

Belfort, J. (2007). The Wolf of Wall Street. New York: Bantam Dell.

Best, G. (2002). Blessed: The Autobiography. London: Ebury.

Cassidy, J. (2002). Dot.Con: The Greatest Story Ever Sold. Allen Lane.

Dash, M. (2010). Tulipomania: The Story of the Worlds Most Coveted Flower and the Extraordinary Passions It Aroused. London: W&N.

Doyle, P. (2008). Value-Based Marketing: Marketing Strategies for Corporate Growth and Shareholder Value (2 ed.). Chichester: John Wiley & Sons.

Goldgar, A. (2008). Tulipmania: Money, Honor, and Knowledge in the Dutch Golden Age. Chicago: University of Chicago Press.

Kay, J. (2016). Other People’s Money: Masters of the Universe or Servants of the People? London: Profile Books.

Levitt, S. D., & Dubner, S. J. (2007). Freakenomics: A Rogue Economist Explores the Hidden Side of Everything. London: Penguin.

Lewis, M. (2010). The Big Short: Inside the Doomsday Machine. New York: W.W. Norton & Company.

Lowenstein, R. (2001). When Genius Failed: The Rise and Fall of Long-Term Capital Management. London: 4th Estate.

Lowenstein, R. (2004). Origins of the Crash: The Great Bubble and its Undoing. New York: The Penguin Press.

Malkiel, B. G. (2016). A Random Walk Down Wall Street: The Time-Tested Strategy for Successful Investing (11th Revised ed.). New York: W. W. Norton & Company.

Pike, R., Neale, B., Linsley, P., & Akbar, S. (2018). Corporate Finance and Investment: Decisions and Strategies (9 ed.). Harlow: Pearson.

Shiller, R. J. (2015). Irrational Exuberance: Revised and Expanded Third Edition (3 ed.). Princeton, NJ: Princeton University Press.

Thaler, R. H. (2016). Misbehaving: The Making of Behavioural Economics. London: Penguin.

Please click/tap your browser ‘Back’ button to return to the location navigated from. Alternatively, click/tap the ‘Antique Keyboard’ graphic below to navigate to The Global Business Strategy Album page.

All content © Colin Edward Egan, 2022